Summary

Volatility will be heightened as we head into 2025, but this can still lead to positive equity outcomes. Meanwhile, although the Fed is unlikely to adjust its easing policy based on actions that have yet to materialise, recent strong US economic data, and the risks of potential tariffs suggest that expectations of a weaker USD and a terminal rate of 3% feel long gone.

What’s top of investors’ minds

1. All roads point to volatility

It isn’t all bad. The last few months of 2024 have proved that volatility/uncertainty will be heightened as we continue into 2025, but this could still lead to positive equity outcomes.

In Asia, the case for Japan remains broadly intact in our view, albeit the gyrations of the yen have created alternating headwinds and tailwinds for companies. In August this was manifested in a tumultuous 48 hours of stock price movement, yet those who ‘sat on their hands’ no doubt continued to see the benefit of a stronger Japan equity market with good further upside.

Recent stimulus in China has seen equity markets rally spectacularly from the third quarter into the fourth, although this followed a pretty disappointing preceding couple of years for stock prices. While many observers are keen for more fiscal stimulus from the government to try and encourage a stubbornly saving consumer into the market, this focus does ensure that China remains part of the ‘Asia dialogue’, critical given its size in the Asia and Emerging Market indices. The imposition of further tariffs looks to be ‘when’ and not ‘if’, but China has diversified it’s trade towards Europe and Asia since the first Trump presidency. Perhaps the bigger ‘what if’ is really around the opportunity for the markets if geopolitics ignites a much greater focus on their own domestic economy.

The second largest economy in Asia, India, in contrast has been racking up month on month equity gains for the last 3 years, however the most recent quarter saw the largest foreign outflows in over 3 years and the Indian market down around 8% in October. That said, domestic mutual fund flows still stood at USD4bn and are an increasingly recurrent bulwark for the market. Of course, you could argue that a correction to Indian equities, given previously lofty valuations, coupled with moderate economic growth in coming quarters could offer further runaway for stock prices to improve. The economy still looks in decent health and a stronger domestic focus could potentially insulate the economy from the incoming President Trump. India also retains the advantage of being a beneficiary of the China + 1 policy.

2. It’s all a matter of style

Whilst the author might be able to remember the days when price discovery was not ubiquitous, investing for the journey – whether via passive, active, value, growth, low volatility strategies and more – sits at the heart of many asset allocation decisions.

It could be counter intuitive but selecting a passive index brings with it certain risks as indices are price and size based so for better or worse, have their own biases. This means that the macro-economic cycle can have an impact on simply allocating to ‘the index’ and geopolitical events can exaggerate this further, within the context where there is decent global growth.

With a second Trump presidency imminent, which will include policies that impact companies around the world, plenty of uncertainty surrounding the course of the Chinese economy and interest rate trajectories in various economies may well support diversity.

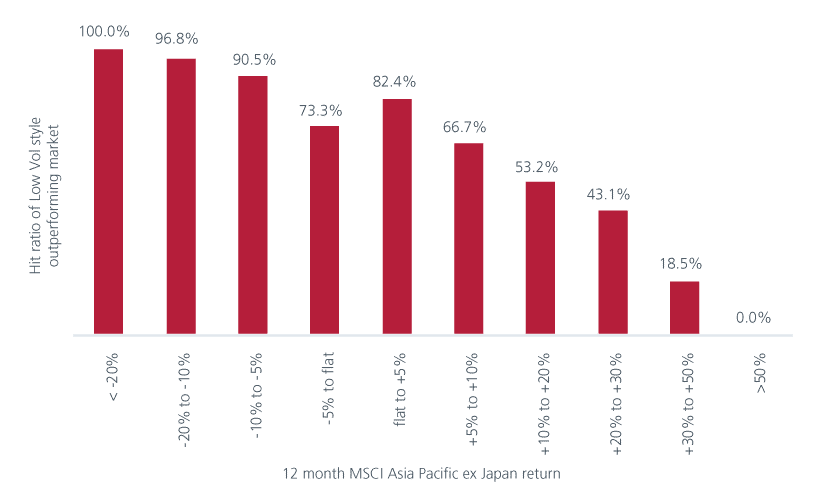

Equity market valuations in Asia and the Emerging markets look attractive although a clear understanding of company fundamentals and likely macro impacts would be key. Low volatility strategies may provide portfolios with a nice downside cushion, as may incorporating a multifactor lens to investing into markets to reduce the momentum and large cap biases of indices.

Fig. Hit ratio of low volatility style beating the market –12-month rolling periods between May 2001 and August 2024.

Data source: Eastspring Investments, LSEG Datastream. * Bloomberg, data from May 2001 to August 2024. The use of indices as proxies for the past performance of any asset class/sector is limited and should not be construed as being indicative of the future or likely performance of the Fund.

3. Can we ‘carry on’ in 2025?

Divergent economies, bouts of inflation and the paths of interest rates could create an intriguing backdrop for the fixed income markets.

A post-election risk-positive backdrop supports narrower credit spreads. The “Goldilocks” scenario—a benign growth outlook with potential stimulus-driven upside surprises, coupled with moderating inflation—creates favourable conditions for carry trades. The era of ultra-low interest rates and quantitative easing may be some way past, yet one only needs to look at the volatile reaction of markets to a stronger Yen in early August to appreciate that the hope of picking up simple returns form interest rate differentials and avoiding FX-related speed bumps remains an attractive way of earning returns, though the unwinding of this can have consequences.

Positive technicals also support credit markets, with limited issuance, elevated base yields, and strong demand from cash-rich investors amid falling cash yields. Prospects of Chinese policy stimulus currently outweigh concerns about US policies targeting China, enhancing the constructive outlook on the Asia credit complex. Recent price action reflects this sentiment. However, given strong year-to-date performance, some participants may seek to lock in gains, potentially leading to minor near-term corrections. The time may be right to rotate out of some Chinese credits with tightened spreads in favour of other geographies less exposed to US policies targeting China.

The potential for inflation from tariffs and increased government spending—leading to a steeper US Treasury curve—cannot be ignored. However, implementing these policies under a new administration could take months to over a year, even with Congressional support, suggesting that positioning for this may be premature. We observe strong market interest in buying duration following the recent yield spike post the US elections, reflecting early-stage biases toward a rate-cutting cycle.

4. What’s next for the Fed in 2025?

Expectations of a weaker US dollar and a terminal rate of 3% feel long gone.

At present, expectations surrounding tariffs and additional fiscal spending remain speculative. The Federal Reserve is unlikely to adjust its easing policy based on actions that have yet to materialise, therefore adhering to the path set since September.

Nonetheless, recent US economic data, including strong labour market indicators, could prompt an upward adjustment in the Fed’s policy trajectory, both in terms of pace and terminal rate. This would, in turn, support front-end yields.

With Trump in the White House in 2025, market expectations have shifted to consider if inflation may once again be a force to contend with, given talk of import tariffs, tax cuts and a crackdown on migrant labour.

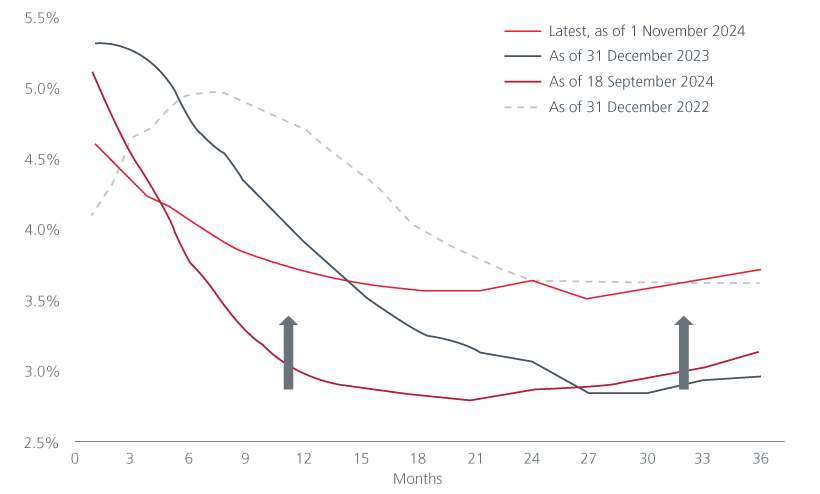

Fig. Fed funds futures forward curves

Data source: LSEG Datastream, Eastspring Investments (Singapore) Limited. The use of indices as proxies for the past performance of any asset class/sector is limited and should not be construed as being indicative of the future or likely performance of the Fund. The latest data provided is as of 1 November 2024.

Please download full report to read more.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).