Executive Summary

- DeepSeek’s breakthrough underscores the immense potential of China’s AI ecosystem, where many companies are trading at much more attractive valuations compared to their US counterparts, even after the recent correction in the US equity market.

- Concerns of a global oversupply of AI infrastructure and hardware appear misplaced, and we see exciting investment opportunities emerging within Asia’s tech and AI supply chains, and even extending beyond the tech sector.

- A value approach does not shy away from growth opportunities but helps us avoid chasing the most obvious but overvalued beneficiaries amid the AI fervour.

The rapid advancements in Artificial Intelligence (AI), especially the breakthrough in generative AI had sparked significant investor interest in AI-related stocks. The exceptional performance of the Magnificent 7 stocks in 2024 was partly fuelled by the AI boom. However, the AI landscape potentially changed forever in early 2025.

On 24th January 2025, DeepSeek, China’s startup AI lab, burst into the mainstream media with their R1 model, purportedly surpassing Open AI’s O1 model at a fraction of the development cost. DeepSeek’s usage of model techniques like Multi Latent Head Attention (MLA) and Mixture of Experts (MoE) lowered the cost of AI inference, reducing the amount of compute and memory needed.

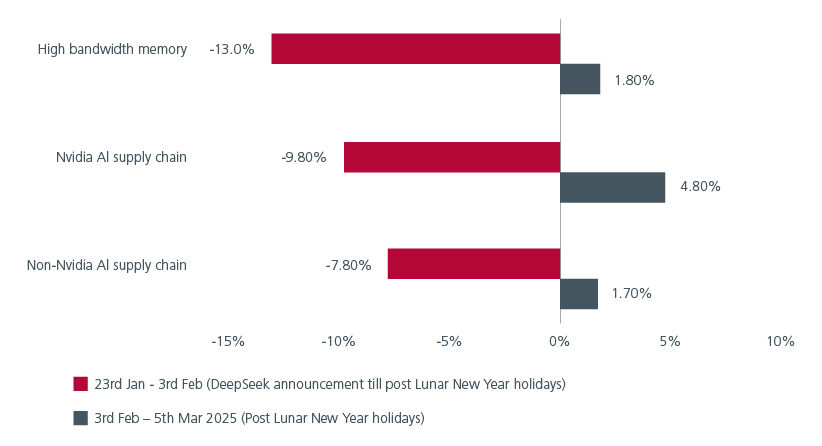

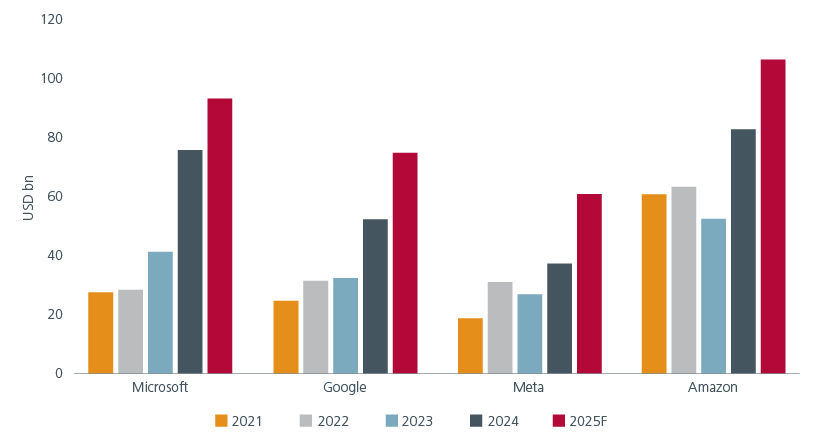

The breakthrough announcement caused a significant sell-off in the AI chip supply chain as investors questioned the need for more AI infrastructure and hardware. However, the supply chain names quickly rebounded after the Lunar New Year period when major US hyperscalers’ (large-scale data centers) guided higher than expected capital expenditure plans for 2025. See Fig. 1. And 2. Our research indicates that major AI frontier model creators were indeed copying DeepSeek techniques but with more powerful compute and memory resources to achieve even faster advancements.

Fig. 1. AI-related stocks fell then rebounded

Source: Bloomberg. As of 5th March 2025. Shows performance of representative baskets of stocks in local currency terms.

Fig. 2. US hyper-scalers are still spending

Source: Visible Alpha 5th March 2025.

Notably, DeepSeek’s advancements underscore the immense potential of China’s AI ecosystem, where many companies are not only innovating rapidly but also trading at much more attractive valuations compared to their US counterparts. We believe that Deepseek’s advancements have far-reaching and enduring implications for Asia, creating exciting investment opportunities within the region’s AI and tech supply chains as well as beyond the tech sector.

A boost for Asian semiconductor and server industries

We expect Taiwan and Korea, home to majority of the AI chip supply chain, to get a significant boost from DeepSeek's advancements. Foundry, backend Integrated Circuit (IC) design, high bandwidth memory (HBM), Chip-on-Wafer-on-Substrate (CoWoS) packaging, Ajinomoto Build-up Film (ABF) substrate, IC testing, server original design manufacturing (ODM), multi-layer printed circuit boards (PCB), liquid cooling are all vital steps and components needed to produce AI servers to meet compute needs.

Advancing China's AI ecosystem

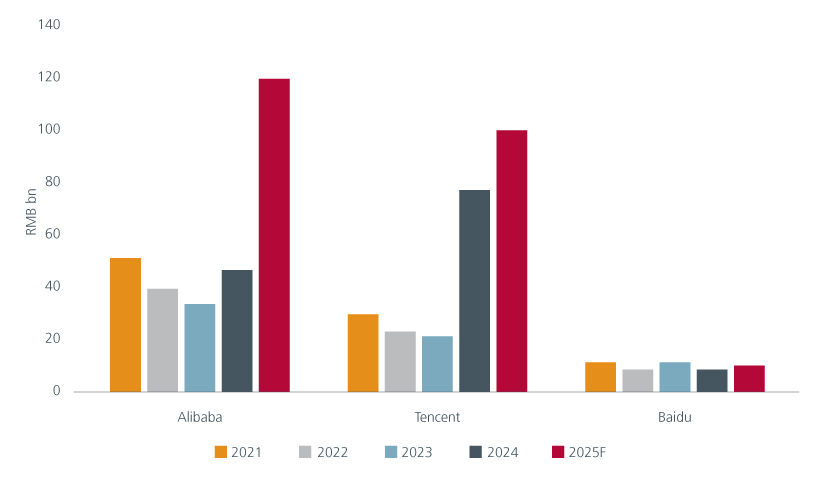

We see Chinese data centers as the immediate beneficiaries of DeepSeek’s breakthrough. China’s cloud service providers have begun offering DeepSeek’s R1 model to both personal and enterprise users. This is sparking widespread experimentation of new software AI features that make use of the R1 models for inferencing. In February, Alibaba stunned the market by forecasting that its AI capital expenditures over the next 3 years will surpass its total spend in the last decade. It is likely that other Chinese hyperscalers will follow suit and significantly increase their capital expenditures to advance their frontier models. See Fig. 3.

Fig. 3. Alibaba announces ambitious AI investment plans

Source: Visible Alpha 5th March 2025, Company guidance. Dotted lines represent Eastspring’s forecast.

China’s semiconductor and server industries, previously limited by US export restrictions, will also gain increasing relevance. These industries had relied on lagging wafer fabrication techniques, but DeepSeek’s model innovations enable the use of less compute-intensive AI chips, potentially giving these industries a new lease of life.

Prior to the DeepSeek breakthrough, Chinese AI development had been lacklustre as it relied on less advanced frontier models trained by inferior chips below US-specified thresholds. This hindered advancements in new applications and AI-aided productivity. DeepSeek’s techniques have removed these barriers and importantly, its AI models are open source - available for all to download, modify and build upon. This openness encourages collaboration and innovation, as users can contribute to improving the models. As a result, Chinese software companies are busy in search of the next killer application/product.

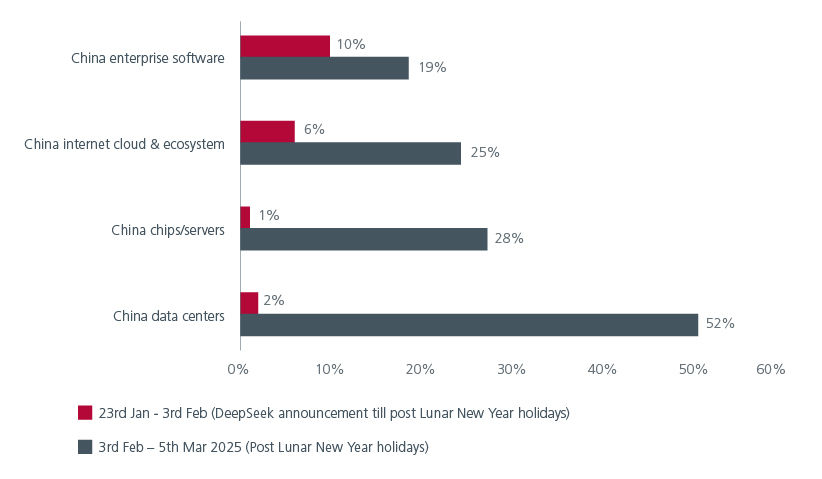

Fig. 4. China AI supply chain players rally

Source: Bloomberg. As of 5 March 2025. In local currency terms. Shows median returns of representative baskets of stocks.

Beneficiaries from edge AI and beyond

The limited compute power of smartphones and PCs has historically kept AI models on these devices to around 7bn parameters in size. DeepSeek however has found a way to use 8-bit floating point (FP8) calculations instead of the usual FP16/FP32, which reduces the computing load without losing too much accuracy. This means we can have larger AI models on our devices and therefore smarter devices.

As such, Chinese smartphone, Taiwanese PC brands and their Asian supply chains should benefit from this development. Lagging edge chips like microcontroller units, power management ICs, Dynamic Random-Access Memory (DRAM) should also enjoy more demand because of this new wave for edge AI devices .1

As AI technology proliferates, the demand for data center resources will rise across the region. Malaysia has already seen significant demand from Chinese companies looking to build presence in ASEAN. Meanwhile, Japan and Korean data center providers are likely to attract interest too, as they are the only 2 Asian countries categorised as Tier 1 in the US AI Diffusion Framework, a set of guidelines and regulations introduced by the US government to manage the global distribution of advanced AI technology. Tier 1 countries have no restrictions for importing advanced AI technology. Meanwhile, the significant energy requirements to operate data centers should also spell opportunities for manufacturers of power generator sets, grid transformers as well as utility companies.

Actively seeking opportunities

Active investing would be required to exploit the opportunities arising from the DeepSeek breakthrough. The stellar returns enjoyed by AI beneficiaries in the US since OpenAI gained widespread attention in early 2023 provide a viable playbook for Asia. To date, selected stocks and sectors have already rallied significantly amid the AI fervour. Against such a backdrop, a value lens helps us to avoid chasing the most obvious but overvalued beneficiaries. Value investing does not shy away from growth opportunities but looks to take advantage of attractively priced growth. Outside of the tech sector, the rising adoption of AI and the large increases in productivity that follow would impact multiple industries, potentially creating new leaders. Deep research and strong industry knowledge would be needed to identify them.

The mention of individual securities or companies in this article is for illustration purposes only and does not imply a recommendation to buy or sell any specific security or financial instrument.

Interesting reads

Sources:

1 Edge AI refers to running artificial intelligence (AI) algorithms directly on devices like smartphones, cameras, or other gadgets, rather than relying on a central server or cloud. This allows the device to process data and make decisions quickly, without needing to send information back and forth to a remote server.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).