Summary

Eastspring’s Multi Asset Portfolio Solutions team anticipates a decelerating albeit positive global growth environment alongside moderating inflation in the next three to six months. Although this might benefit equities in the short term, the team is tactically cautious on global equities due to stretched valuations, potential data disappointments, and increased volatility. Meanwhile the looser monetary policy stance in developed markets presents a constructive backdrop for high-quality bonds.

This is an extract of our Q4 2024 Market Outlook. Click here to download the full report which includes a special feature “Gold continues to shine”.

Macro: Odds of a “Goldilocks” outcome improve post the Fed rate cut, yet risk of a US recession lingers

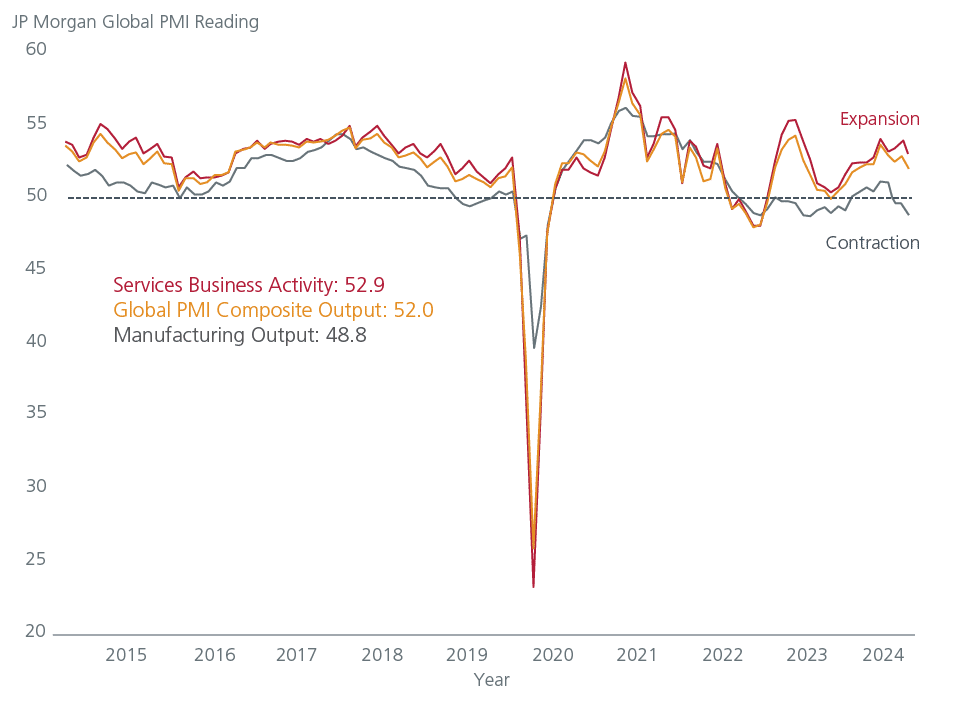

The global economy has been expanding steadily for the past 11 consecutive months, as shown by the J.P. Morgan Global Composite Purchasing Managers’ Index (PMI) Output Index. However, a closer analysis indicates that the global growth momentum is decelerating. Moreover, a widening gap between the stronger service sector and the weakening manufacturing sector underscores the increasing unevenness in growth.

Global Purchasing Managers’ Index (PMI)

Source: LSEG Datastream, Data is as of September 2024 end.

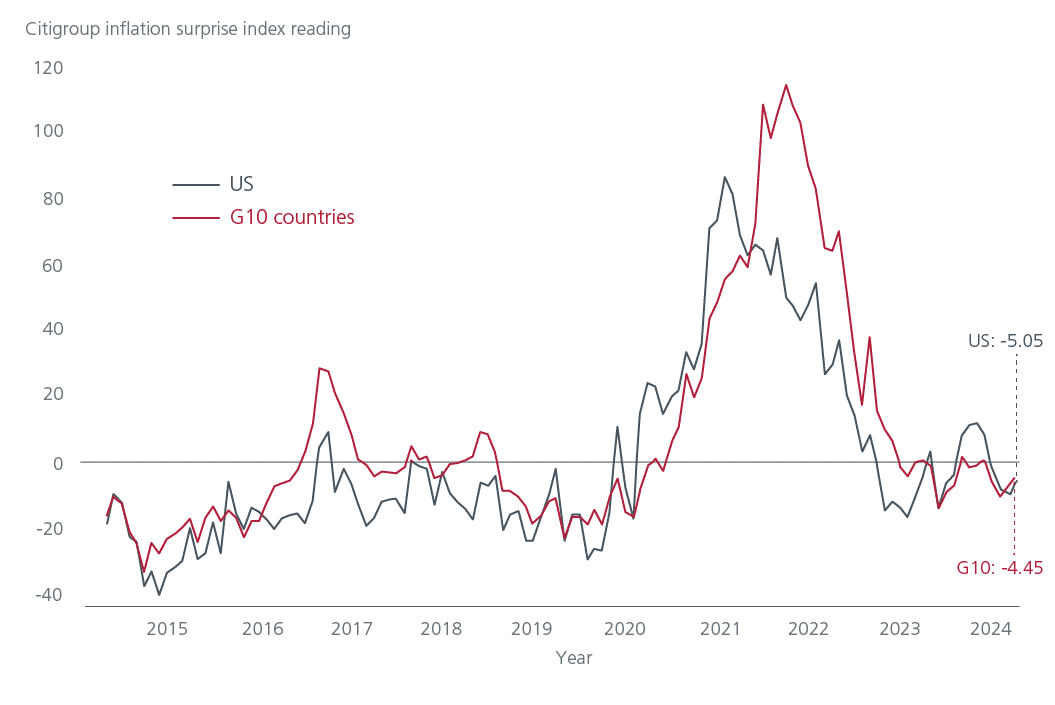

Both the monthly and annual headline US consumer price inflation rates have been on a noticeable declining trend and progressing towards the Fed's 2% target. Nonetheless the path towards this target may be uneven; core US CPI remains relatively persistent due to the still elevated shelter inflation component, though we believe this will reverse course in due time.

Citi Inflation Surprise Index (US, G10)

Source: LSEG Datastream; Citigroup. Data is as of 30 September 2024.

The team continues to monitor the US labour market and wage growth conditions to detect any big shifts in the inflation expectations. Additionally, the team is looking out for any potential supply-side driven inflation risks, arising from escalating tensions in the Middle East.

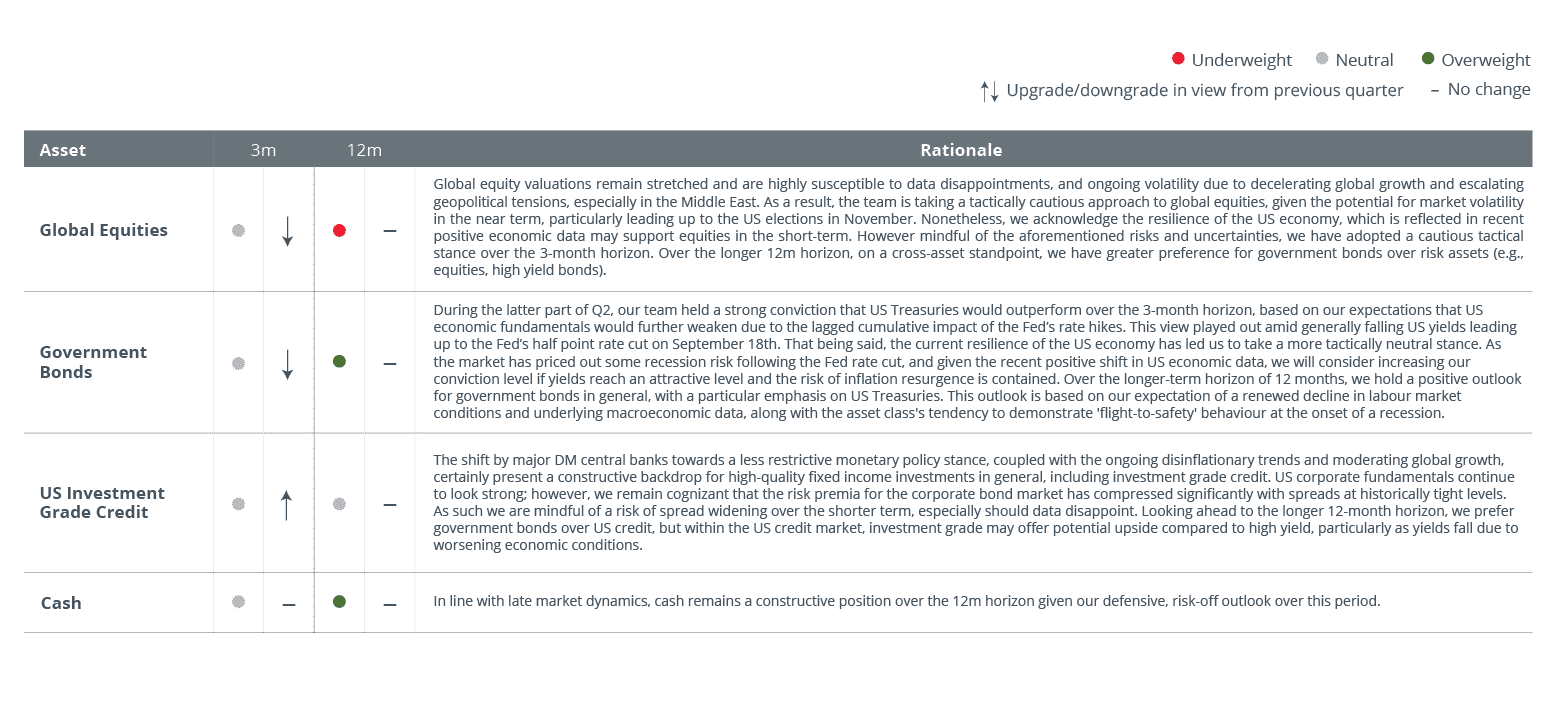

Asset Allocation: Staying tactically defensive due to expected volatility and potential data disappointments

Given the upcoming US election, the release of the October US employment report, the Fed meeting in early November, and escalating geopolitical tensions in the Middle East, we anticipate heightened market volatility to persist in the near term. Moreover, global equity valuations remain lofty and are vulnerable to data disappointments. While US economic data has been resilient, we believe that the risk of a recession is currently undervalued. As such the team is adopting a more cautious tactical stance for risk assets over the 3-month horizon.

Over the longer-term horizon of 12 months, the team has a greater preference for government bonds, especially US Treasuries, over risky assets (e.g., equities, high yield), in line with late economic cycle dynamics and the asset class’s appeal in the event of a recessionary environment.

Datasource: Multi Asset Portfolio Solutions team. Asset class views are as of the team’s most recent monthly meeting in early October 2024 and should not be taken as a recommendation.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).