Executive Summary

- Many of Japan’s small and mid-cap companies can easily improve their return on equity by using their net cash for share buybacks

- Higher share price performance of companies that disclose improvement plans will nudge more small caps to adopt balance sheet reforms

- The small and mid-cap segment is a prime market for longer term valuation-driven stock pickers; many of them are currently trading below their book value

In the previous article, we stated key factors that will continue to support Japan’s stock market. These include the ongoing corporate reforms, the revamped savings policy which will spur investments, and the fact that Japan remains cheap versus its global peers despite the re-rating. Supportive fiscal and monetary policies and expectations of a reflationary environment have also underpinned the market. As it happens, Japan equities hit another record high in March.

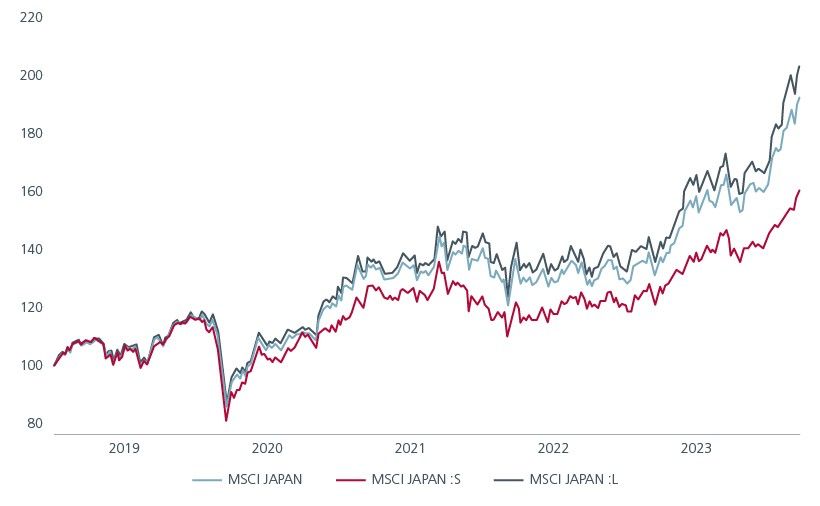

The rally, however, has mostly been driven by large cap stocks. See Fig 1. This is likely the result of index buying by various groups and investors shifting out of China. Japan’s small caps however have not moved in tandem. Globally, small caps have seen muted rises; small caps in the US have also lagged large caps since 20201.

In Japan, the current trade discount of small to large caps is at an extreme level. The last time such extreme widening took place in 2007/08. Subsequently there were 10 years of particularly good performance for small caps. Typically, as seen in the past 30 years, when the valuation cycle widens to this extreme, it tends to snap back.

Fig. 1: Japan’s small caps lag in returns

Source: LSEG Datastream, MSCI indices as of 26 Mar 2024

Small caps are the largest potential beneficiaries of reforms

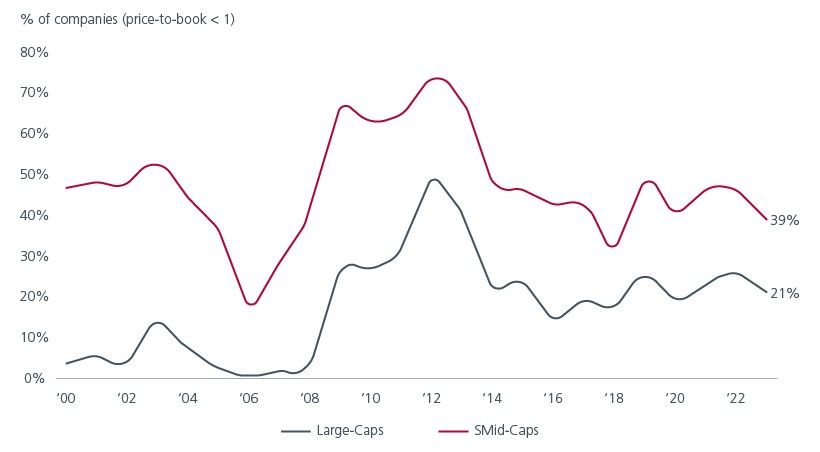

Unlike the large caps, the momentum has not taken off for Japan’s small to mid-caps (SMIDs). But once it does, it can offer equally attractive returns. We believe the impact of the Tokyo stock exchange (TSE) reforms will be a key trigger to unlock value in the SMIDs. There are far more of them in terms of absolute numbers of companies in the small to mid-cap space compared to large caps. A higher proportion of SMID stocks are trading below book compared to large caps. See Fig 2.

Fig 2: 39% of Japan’s SMIDs trade below book value

Source: Eastspring Investments, Japan large and small to mid-cap stocks data based on Bloomberg, LSEG Datastream, Factset, and J.P. Morgan calculations as of 31 Dec 2023. All yearly values are as of beginning of year.

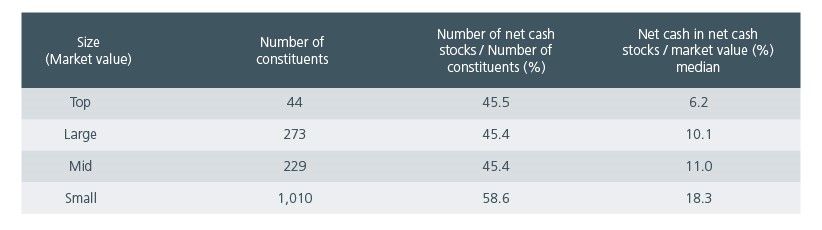

Hundreds of SMIDs also have solid balance sheets with net cash to market capitalisation as high as 70%. Fig 3 indicates the breakdown in the Russell/Nomura index of the percentage of companies with a net cash position categorised by market capitalisation; 58% of the small caps have net cash on balance sheet compared to 45% in large and mid-caps. Furthermore, the net cash in small cap stocks with net cash is about +18% of their market value. This level of cash facilitates easy share buybacks which in turn will improve the return on equity (ROE).

Fig 3: Higher proportion of small cap companies with net cash

Source: Nomura based on Russell/Nomura index - includes top, large, mid and small cap (ex-financials) as of Mar 2024

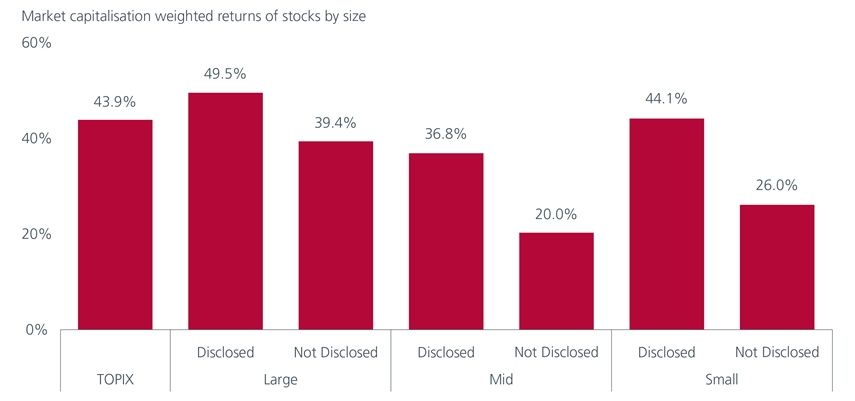

TSE’s corporate governance reforms have already nudged multiple large cap companies to act to improve ROE. The share price performance of companies that disclose is higher. See Fig 4. The disparity was even wider in the small cap space. The pressure to disclose is growing. It is a matter of time before the SMIDs follow suit.

Small caps’ attractive valuations, high net cash levels and share price performance disparity versus large caps are key reasons why this group will be the largest potential beneficiaries of the TSE’s initiative. Every day seems to bring new positive news on balance sheet related reform for these companies.

Fig 4: Performance gap between the disclosed and undisclosed group

Source: Refinitiv, UBS. Performance is measured between end-2022 and 18 Mar 2024

Reflationary backdrop favours SMIDs

Investors have also become more optimistic about Japan’s economy on signs of healthy inflation in recent months. The Bank of Japan ended eight years of negative interest rate policy and raised the policy rate to +0.1% in March after the recent annual wage negotiations yielded the biggest pay hikes in 33 years. An inflationary environment means consumers and private sector players with huge cash savings will mobilise those into consumption and investment. In fact, the inflationary cycle favours small caps more so than big caps as more of SMIDs tend to be tied to the domestic economy.

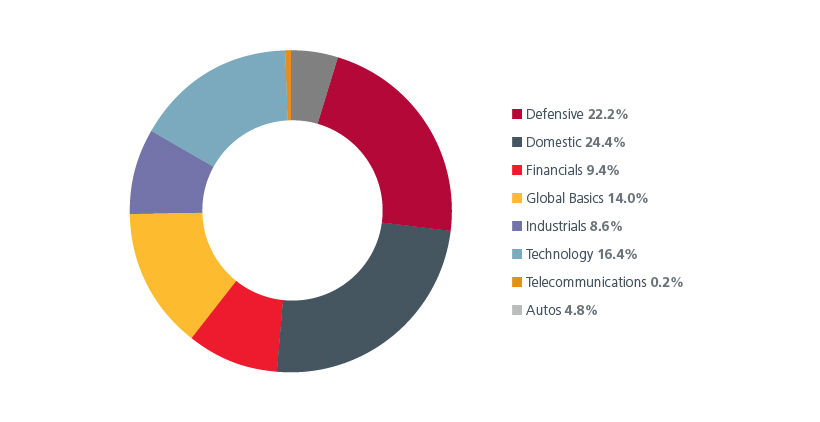

That said, there is a wide and diverse universe of stocks in the SMID cap space. Domestic and export related companies are distributed widely across a range of industries. See Fig 5. As such an investor can enjoy diversification benefits by investing in SMID caps. Ultimately, measures to help companies re-shore manufacturing bases will lift Japan’s economy, spur higher wages, and rekindle domestic consumption.

Fig 5: SMID cap wide and diverse investment universe

Source: Eastspring Investments, as of 31 December 2023. Sector weight for the Russell Nomura Mid-Small Cap, internal classification

Active investing uncovers alpha

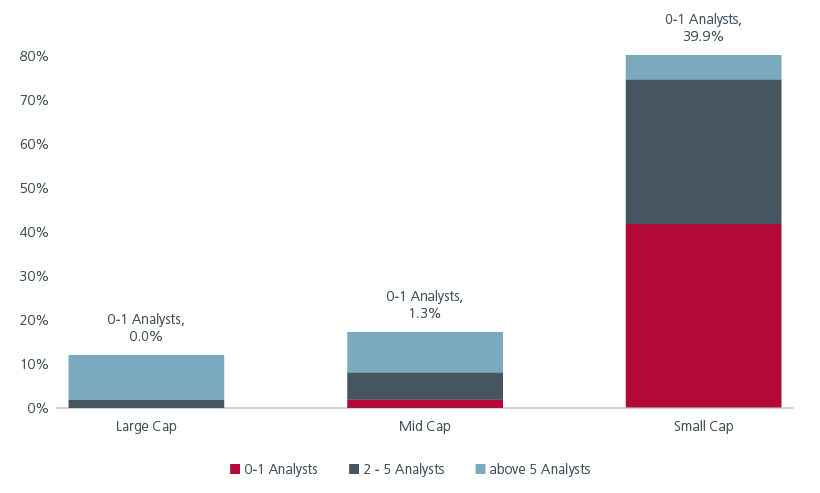

The triggers are in place for the SMIDs to rally. To reap the full benefits an active investment approach works best. The SMID space is a prime market for longer-term valuation-driven stock pickers. Although small cap stocks represent approximately 65% of the Japan universe2, they are often under researched. The amount of sell-side analyst coverage is a good proxy for the market’s focus. Within the TOPIX Index, under covered small cap stocks represent almost 57% of the index. See Fig 6.

We repeatedly see cases where smaller companies not only fall out of favour, often for shorter-term thematic reasons, but are also dropped from analyst coverage altogether. This drives mispricing to the sort of extremes where good or improving companies are simply ignored. Given that our investment process relies on exploiting persistent behavioural biases, this is a very good thing for us.

Fig 6: Limited sell-side coverage for SMID cap stocks

Source: Eastspring Investments, Nomura, based on IFIS and MSCI data, as of 1 April 2022. The universe data is based on the MSCI Japan Large Cap Index, MSCI Japan Mid Cap Index and MSCI Japan Small Cap Index. *Represents stocks with 0-1 Analysts covering the stock.

Within the SMID space, we see opportunities in undervalued regional banks and retailers. The former has a big domestic loan book and will benefit as rates edge up. Retailers will benefit as they pass on higher costs to more “cash-rich” consumers. In addition, we see value in stocks that have been sold off indiscriminately due to weak sentiment; these include semiconductor and mobile phone players. Equally we avoid some stocks that are heavily exposed to China i.e., commodity and auto companies.

Our investment process is based on the understanding that the greatest opportunities are likely to be found where the market’s shorter-term preferences and extrapolation have caused a large dislocation between the price and relative value of a company. This approach allows us to invest in companies that are likely beneficiaries ahead of analyst’s recommendations.

Access expert analysis to help you stay ahead of markets.

- Follow

-

-

-

Interesting reads

Sources:

1 MSCI US Large Caps and MSCI US Small Caps as of 26 Mar 2024

2 Stocks with a market cap below 100 Bn Yen. Russell/Nomura index as of Mar 2024

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).