Eastspring Investments

Feb 2025 | 5 min read

Summary

- India remains one of the fastest-growing economies, with IMF projecting 6.5% growth in FY26 and FY27, outpacing other large economies

- India's 2025-26 budget and RBI's rate cut aim to boost consumption and capex, supporting fiscal discipline and sustainable growth

- India's political stability ensures policy continuity while strong demand for Indian equities by institutional and retail investors will underpin the market

India’s economy is projected to grow by 6.4% in the financial year ending March 2025, the slowest in four years. This downturn can be attributed to weak consumer demand, sluggish private investment, and lower government expenditure due to election-related spending curbs. While the slowing growth has dented confidence and highlighted India’s vulnerabilities, it is crucial to assess India’s future growth in the global context instead of focusing on the most recent performance.

India continues to be one of the fastest growing economies of the world. According to IMF estimates, the Indian economy is likely to grow at 6.5% in FY26 and FY27. No other economy of comparable size is likely to grow faster than India over the next few years.

Slowdown appears to be transient

This moderation in growth should also be seen in the light of an unfavourable base effect post the Covid. As the pandemic restrictions were removed, pent up demand for services and higher production turbocharged India’s economic growth. The Indian government also ran higher deficits during and post pandemic which fostered the government capex-led growth. Hence to a certain extent, it can be said the economy is reverting to trend growth.

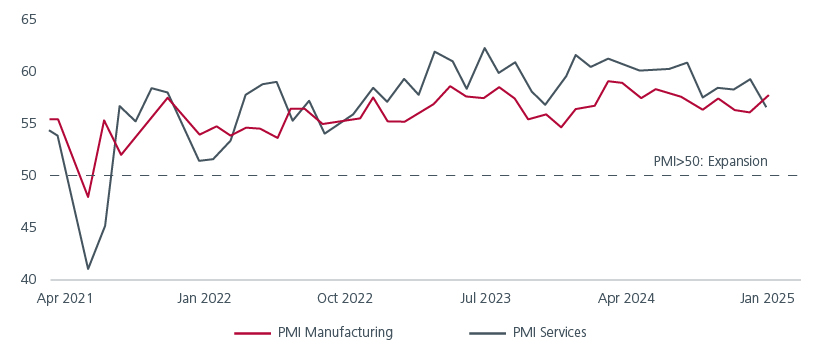

There are also signs of improvement in manufacturing activity; the Purchasing Managers Index rose to 57.7 in January, up from 56.4 in December and 56.5 in November. The services PMI however declined. With regards to consumption the recovery in rural demand is being supported by improved agriculture indicators. Meanwhile urban demand is expected to get a fillip from the latest budget.

Fig 1: Manufacturing PMI shows improvement

Source: BofA Global Research, Haver, Jan 2025

Consumption and capex get a boost

India’s 2025-26 budget offers policy continuity and outlines a roadmap to attain sustainable growth. It incentivises job creation, supports discretionary incomes and provides a blueprint to navigate through rapidly changing global macroeconomic conditions and business environment. The tax savings will offer a boost to discretionary consumption while real estate investment across micro-markets may benefit from tailwinds. The rejig in customs duties is also positive for India’s manufacturing ecosystem.

Despite the focus on accelerating consumption, allocations to key capex intensive sectors such as railways and road transportation remain high. The next leg of growth will be driven by state owned enterprises and private capex. A sustainable rise in consumption bodes well for private sector capex over the medium term. It is also worth noting the government has adhered to its fiscal consolidation stance, hinting at greater fiscal discipline.

Close on the heels of the budget and the Reserve Bank of India’s (RBI) recent liquidity injections into the system, the RBI has for the first time in nearly five years cut the key repo rate by 25 bps from 6.5 per cent to 6.25 per cent, to provide additional stimulus to the sluggish economy. The combined fiscal and monetary stimulus should spur consumption and credit creation going forward.

The equity premium justification

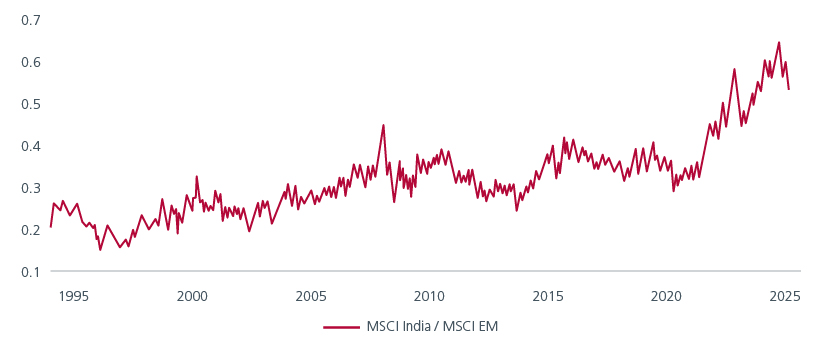

Lured by the country’s high economic and superior earnings growth in the post Covid period, investors piled into Indian equities. As a result, India’s outperformance versus Emerging Markets (EMs) became more pronounced since late 2020. See Fig 2. However, since September 2024, foreign investors started to pull out, spooked by the slowdown in the economy.

Fig 2: India outperforms EMs in the long term

Source: LSEG Datastream, MSCI indices, 4 Feb 2025

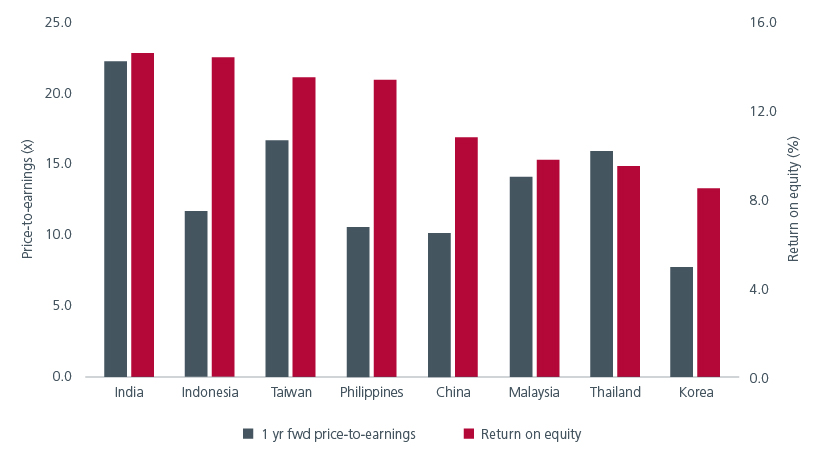

Global headwinds and high equity valuations too affected foreign investors’ sentiment. That said, India’s valuation premium can be justified if one considers a few factors. A key point is that India’s return on equity (ROE) is amongst the highest. See Fig 3. India also ranks second worldwide, just behind the US, in the number of companies that have consistently achieved a ROE exceeding 20% for over a decade.1

Fig 3: India is expensive for a reason

Source: PruICICI, Morgan Stanley, 31 Dec 2024

Consistent ROE performance typically reflects the underlying financial health of companies. Still, companies with high valuations have to continue to deliver better earnings. After being in the fast lane for three years, earnings numbers saw some deceleration in Q1 and Q2 FY25.

The recent Q3FY25 numbers suggest a mixed bag. Out of the 242 companies, better earnings were reported by companies in the financial sector. Amongst the non-financial companies, revenue and profit after growth remains weak on a year-on-year basis but the quarter-on-quarter data is encouraging and suggests that an earnings recovery might be already underway.

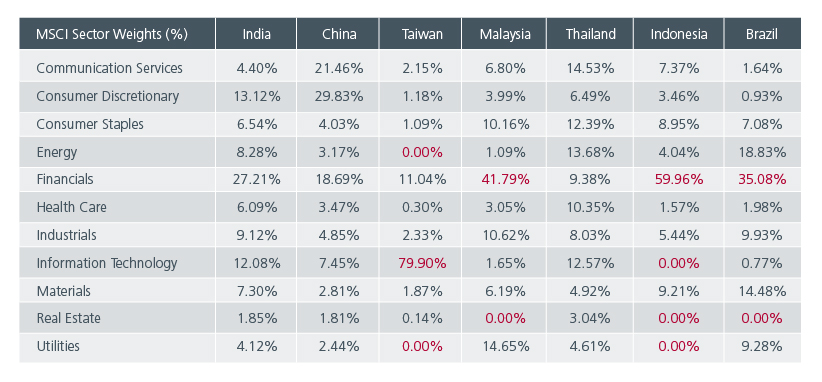

All said, India offers a huge domestic market where there is under penetration of consumer goods as well as well-regulated capital markets that offer depth, diversification, and liquidity. So, this is where an active investment strategy is best placed to pick the potential winners. For now, the risk return trade-off favours large caps over mid and small caps.

Fig 4: India remains one of the most diversified markets in EMs

Source: MSCI factsheets, 31 Dec 2024

Considerable potential to be harnessed

2025 will undoubtedly be a challenging year. US President Trump’s transactional approach to trade can impact global growth and the US administration’s policies are likely to trigger intermittent market volatility as seen in the recent market movements to tariff announcements. Nonetheless India is unlikely to see major dislocations. The country should continue on a growth path with occasional cyclical blips.

India's near-term political stability ensures policy continuity and certainty. The country is beginning to integrate more into global supply chains, with significant potential yet to be utilised. Over the next 5-10 years, India is expected to scale up production and export of electronics goods. Key sectors like automobiles, chemicals, and pharmaceuticals are also part of the global supply chain. Additionally, logistics costs in India are likely to decrease, making them globally competitive. This indicates a strong growth potential for India's participation in the global supply chain.

Meanwhile India’s thrust on startups and innovations makes it a unique place for global players looking to diversify their manufacturing base. Startups contribute ~15% to Indian economy. India’s start up ecosystem is the third largest in the world, valued at ~USD 349bn.2 In 2024, India was Asia Pacific’s bright spot for initial public offerings (IPOs), delivering a 152% increase in IPO proceeds to USD16.8bn.3

Last but not least, Indian markets remain firmly underpinned by domestic inflows. The continued strong demand for Indian equities by institutional investors and retail investors are soaking up the outflow of foreign capital. This should continue to provide support for India’s equity market.

The article includes insights from ICICI Prudential Asset Management

Access expert analysis to help you stay ahead of markets.

- Follow

-

-

-

Interesting reads

Sources:

1 https://www.ibef.org/news/india-second-only-to-u-s-in-number-of-consistent-high-performing-companies-report

2 https://assets.kpmg.com/content/dam/kpmgsites/in/pdf/2024/12/exploring-indias-dynamic-start-up-ecosystem.pdf

3 https://www.pwc.co.uk/services/audit/insights/global-ipo-watch.html

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).