Summary

We enter 2025 being constructive on higher yielding credit and global equities on a tactical basis. From a medium-term perspective, the world has become increasingly unpredictable in 2025 due to policy uncertainty. As such, maintaining a disciplined approach to portfolio risk is just as important as focusing on investment strategies, particularly as Trump's policies begin to impact the market post-inauguration.

1Q 2025 Market Outlook: Trump 2.0 - A test of market and economic resilience

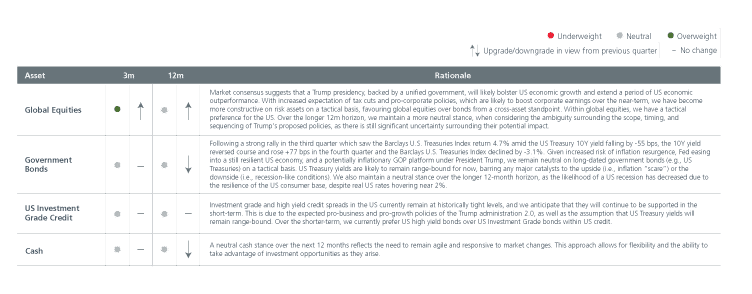

Market consensus suggests that a Trump presidency, backed by a unified government, will likely bolster US economic growth and extend a period of US economic outperformance. With increased expectation of tax cuts and pro-corporate policies, which are likely to boost corporate earnings over the near-term, we have become more constructive on risk assets on a tactical basis, favouring global equities over bonds from a cross-asset standpoint.

This is an extract of our Q1 2025 Market Outlook. Click here to download the full report which includes a special feature “Trump’s tariff tango: Assessing the impact”.

Macro: Trump 2.0 policies to present challenges (and uncertainty) to “U.S. exceptionalism” in 2025

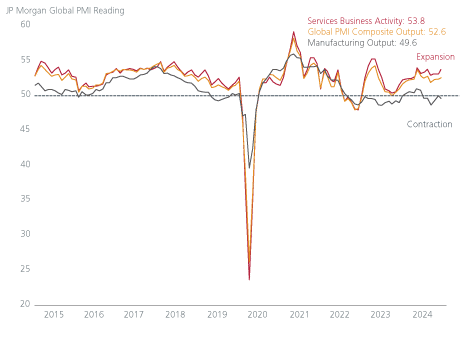

The J.P. Morgan Global Composite PMI Output Index has remained above the '50' boom-bust line for fourteen consecutive months, indicating ongoing global economic expansion.

The US economy continued to be a key driver of global growth and had displayed its “exceptionalism” throughout 2024. At this juncture, assuming the US economy continues to operate above potential, the odds of a no-landing scenario (i.e., continued overheating) have increased.

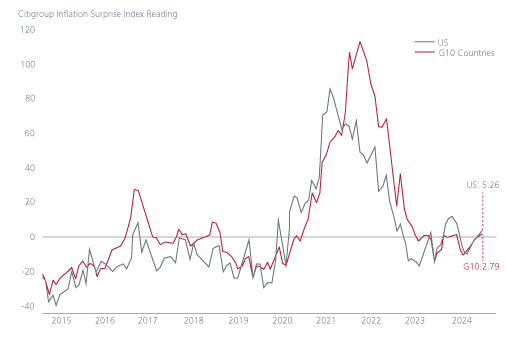

The US core Consumer Price (CPI) Index data for December 2024 showed positive progress, with shelter inflation - a notable portion of the core CPI basket - showing its smallest annual increase since January 2022. Though the trend is encouraging, we acknowledge that the potential inflationary impact of Trump’s various policies - especially tariffs - remains uncertain over both the short- and long-term. We believe that US inflation has generally been on a downward trajectory overall, especially compared to the reflationary first quarter of 2024.

To detect any signs of a reacceleration in inflation, we are closely monitoring labour market conditions and wage growth trends. Additionally, we remain mindful of any potential supply-side driven inflation risks that may arise from escalating geopolitical tensions.

Asset Allocation: While continued US exceptionalism may be hard to ignore, diversification remains relevant as ever

We are entering 2025 on a positive note. The US economy has expanded at a faster than expected pace in 2024, and the labour market remains robust, defying the impacts of tighter monetary policy implemented over recent years.

As such, we are constructive on higher yielding credit and global equities on a tactical basis. We are currently cautious on US Treasuries given the resilience of the US economy, which may disrupt the Fed’s easing cycle, as the odds of a US recession are decreasing and shifting towards inflationary growth.

From a medium-term perspective, the world has become increasingly unpredictable in 2025. For example, forecasts for US real GDP growth range from 0.5% to 2.9% for this year, as economists are uncertain about which policies President Trump will prioritise and the order in which he will implement them.

At this juncture, we believe that maintaining a disciplined approach to portfolio risk is just as important as focusing on investment strategies, particularly as Trump's policies begin to influence the market post-inauguration. As such, active risk management and diversification across various assets remain key.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).