Executive Summary

- With tariff headlines expected to lift market volatility in 2025, the attractive yields and steady income stream from high quality Asian bonds should appeal to investors.

- The region’s stable macro fundamentals and net negative supply of corporate bonds in 2025 should underpin the Asian bond market. Credit selection will be key in driving alpha generation as tariffs produce winners and losers.

- Dispersion will remain high among local currency bond markets. Investors can unlock significant value by capitalising on market dislocations, leveraging Asian central banks’ rate cut cycles and navigating geopolitical risks.

Asian bonds, as measured by the JP Morgan Asia Credit Index (JACI), have delivered positive returns year to date, following strong returns in 20241. US and Asian bond yields had initially risen post the US election as the market focused on the prospects of stronger US economic growth, higher inflation and bigger US fiscal deficits. US 10-year Treasury yields hit a high of 4.8% in mid-January 2025.

The market narrative has shifted since Trump’s inauguration. Concerns about large-scale deportations potentially impacting US growth exceptionalism contributed to a decline in US Treasury yields. Additionally, the initial delay in implementing tariffs, along with a more universal application of tariffs beyond just targeting China, led to a relief rally in Asian bonds.

However, tariff risks are delayed, not eliminated. While equity and bond market volatility has been relatively subdued to date, higher volatility cannot be ruled out when markets refocus on tariffs in the coming months. High quality Asian bonds offer investors the opportunity to lock in attractive income streams that can help temper portfolio volatility. Given tight spreads and a shallower than expected US rate cutting cycle, carry would be key for bond returns in 2025.

Navigating tariffs in Asia

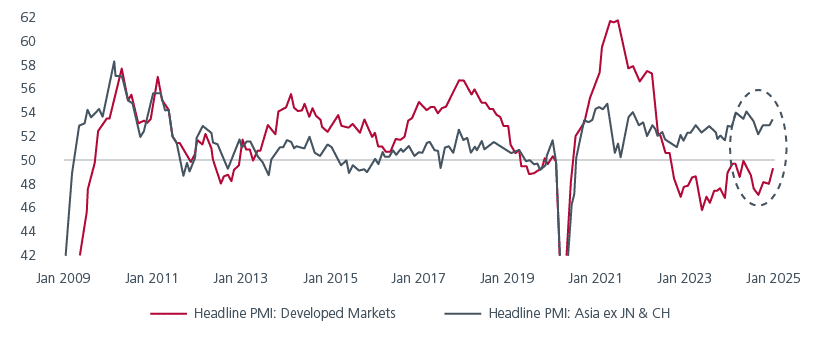

Asian economies, with the exception of China, have held up well despite rising geopolitical tensions and tariff uncertainty. See Fig. 1. The latest readings of headline manufacturing and new orders PMIs in most Asian countries are above 50, signalling expansion.

Fig. 1. Manufacturing PMIs: Developed markets vs Asia ex Japan & China

Source: S&P Global, CEIC, HSBC. CH refers to mainland China and DM refers to US, UK, Eurozone and Japan. 4 February 2025.

Tariffs will impact Asia by delaying capital spending decisions and dampening corporate confidence, potentially hurting economic growth. There are various ways to estimate tariff risk, such as the percentage of exports to the US, trade surpluses with the US, and net tariff rates. Secondary effects on economies closely tied to those in the US direct line of fire also matter. While many Asian economies might be affected, there will be nuances. For example, economies with Free Trade Agreements with the US could be less impacted. Strategic relationships with the US may also offer some countries (e.g. Japan and potentially India) greater leverage, and economies like Taiwan, Korea and Singapore, which produce complex exports, could enjoy more inelastic demand. In-depth credit research is necessary to understand the transmission mechanisms as well as direct and indirect implications on bond issuers. For now, Trump’s recent tariffs on steel and aluminium seem to have a limited impact on Asia.

Meanwhile, we would caution being overly bearish China. Its share of US imports has fallen since the first Trump administration, making it less vulnerable. Chinese policymakers also appear to be increasingly willing to provide stimulus and other supportive measures. With market pricing still reflecting extreme investor pessimism towards China, there could be opportunities for investors to position themselves for a recovery. Catalysts for a market turnaround include reduced tariff risks and increasing fiscal stimulus.

Opportunities in USD and local currency bonds

The credit fundamentals of Asian corporates have remained largely stable with the average debt to capital ratio on a downward trend. We are positive on the fundamental outlook for the internet, telecoms, transport and consumer sectors. We also like Australian and Japanese financials.

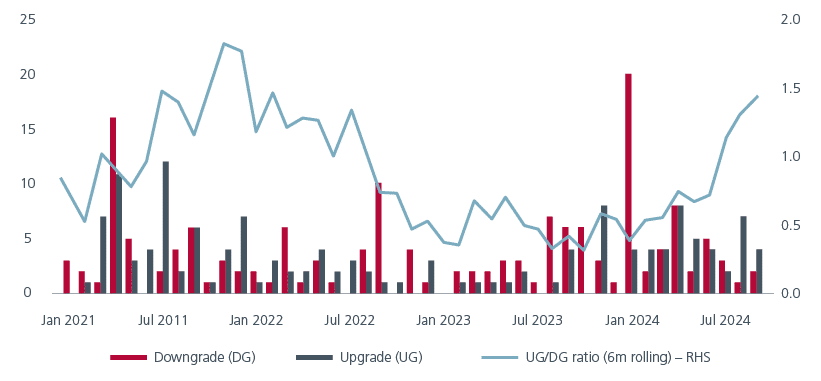

Within Asian USD-denominated bonds, we prefer to invest in investment grade (IG) bonds as tight credit spreads do not compensate investors adequately to take on more risk. We are staying defensive and we look to re-engage when spreads widen. Notably, there has been more upgrades than downgrades among Asian IG bonds in recent months. See Fig. 2.

Fig. 2. Asia IG has seen more upgrades than downgrades in recent months

Source: JPM. January 2025.

We look for opportunities to extend duration when yields spike, but for now, shorter duration credits pay us for waiting and they offer ample liquidity should risk aversion rises. Within Asian IGs, AA and BBB-rated bonds appear to offer better value.

On the supply front, higher for longer US rates are likely to curb USD bond issuances from Asian corporates. The net negative supply of USD-denominated Asian corporate bonds expected in 2025 will also be supportive of the market.

Within Asian local currency bonds, market dislocations, primarily driven by tariff-related uncertainties, have created rare valuation opportunities, although Asian currencies have also weakened. We believe that select Asian local bonds, hedged back into USD, offer attractive opportunities for professional investors to boost portfolio returns.

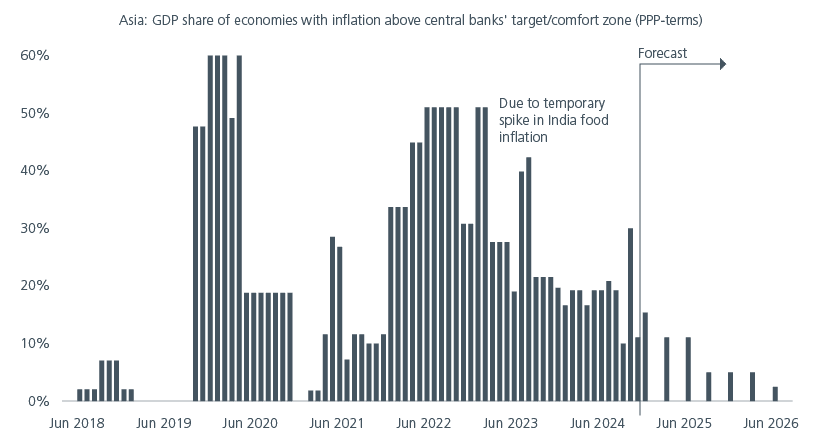

While inflation remains sticky in the US, inflation is trending towards central bank targets in most of Asia. See Fig. 3. With tariffs presenting downside risks to the region’s growth, we believe that Asian central banks are more willing to cut rates to support growth, even if the US Federal Reserve holds. On this note, central banks in India, Indonesia, Korea and Singapore have already cut rates or signalled further easing.

Fig. 3. Domestic inflation has already returned to central banks’ comfort zones

Source: Haver, Morgan Stanley Research. January 2025.

Some Asian central banks have also been deploying foreign exchange reserves to limit downside risks, providing a stable environment for high-yielding local bonds. Over the past three years, Asian high yielders like India and Indonesia have delivered strong returns, supported by central bank policies. The steep yield curves of these high-yielding local bonds offer opportunities before further rate cuts materialise.

Unlocking income and enhancing returns

Asian economies excluding China have been relatively resilient to date and Asian central banks appear willing to cut rates to support growth if needed. Supportive macroeconomic conditions and a negative net supply of Asian corporate bonds in 2025 should help underpin the Asian bond market. With tariff headlines expected to lift market volatility in 2025, the attractive yields and steady income stream from high quality Asian bonds should appeal to investors.

Given tight spreads and a shallower than expected US rate cutting cycle, carry would be a key component of total returns. With tariffs likely to produce winners and losers, credit selection will be important to drive alpha generation. Investors will need to stay agile and disciplined to navigate the year successfully.

The idiosyncratic drivers across the region suggest that dispersion will remain high among the local currency bond markets. By taking advantage of market dislocations, leveraging Asian central banks’ rate cut cycles and managing geopolitical risks, investors can unlock significant value and enhance portfolio returns.

Access expert analysis to help you stay ahead of markets.

- Follow

Interesting reads

Sources:

1 19 February 2025. JACI returns in USD. Bloomberg.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).